What is blockchain?

Ask someone what blockchain is and chances are, you’ll get an inquisitive response rather than a straight answer. Something along the lines of “Something to do with Bitcoin?”

Google trends shows that people first started searching ‘blockchain’ back in 2013 - that’s five years after it was referenced by Satoshi Nakamoto, the mysterious person or group who authored the original Bitcoin white paper. Searches consistently increased up to mid-2017, and absolutely exploded from Summer 2017 until the end of the year (in line with when Bitcoin’s value peaked).

Many of us have heard of it, some of us might even have gone as far as to invest in cryptocurrency, but even then, there’s a strong likelihood you still don’t know what blockchain is (you’re not alone)! In Busan, South Korea, a government designated “blockchain regulation-free zone”, intending to stoke regional blockchain development resulted in a reported 62% of the cohort admitting to not understanding what blockchain technology really is.

Despite this, the blockchain industry continues to develop at a blistering rate for those projects with a clear vision and use case. Switzerland’s Crypto Valley, based in Zug, is an example of a successful for-blockchain regulatory environment where projects teams are encouraged to intermingle and grow. Zug has even integrated blockchain into civic life, having successfully trialed blockchain-based e-voting.

If you’ve ever had an interest in new technologies, blockchains or cryptocurrencies, it’s a good idea to get clued-up on a few new phrases and concepts. A basic understanding of blockchain can open up the world of decentralised finance (DeFi), ‘smart’ contracts and so much more!

So, what is blockchain?

It can help to cast aside all prior notions about Bitcoin and start with a blank slate. While similar technologies have existed for decades, blockchain, as it’s been popularised, was originally designed for Bitcoin and is the conceptual foundation upon which most cryptocurrencies operate. However, blockchain is a novel record-keeping technology that has applications far beyond just digital currencies.

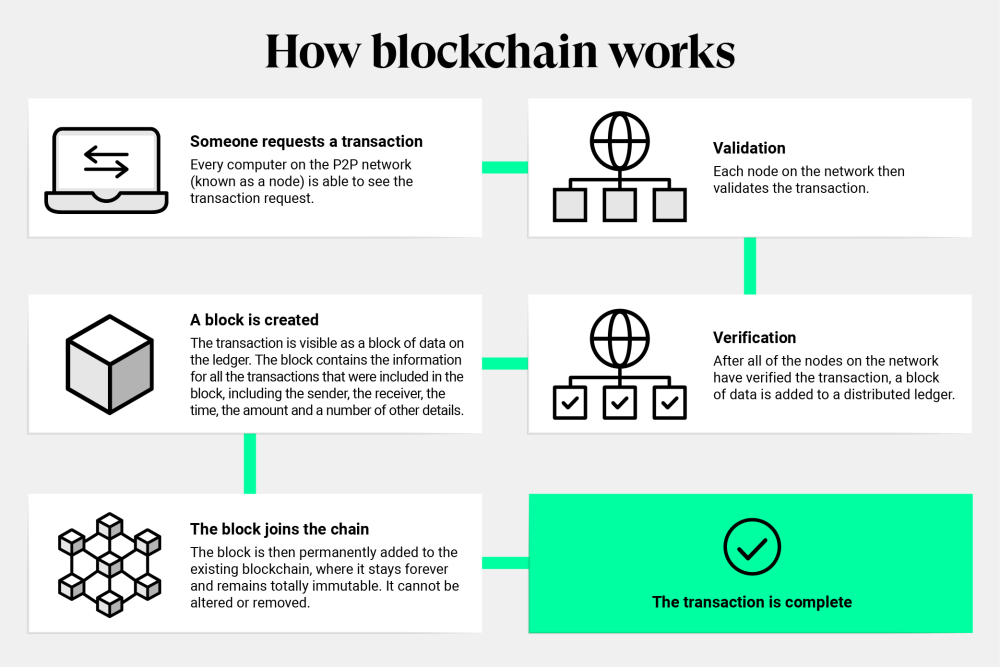

A blockchain is a transparent and decentralised database (called a distributed ledger) which keeps track of every single peer-to-peer transaction, in real time. Transparent in the sense that anyone can view a public blockchain. Decentralised in that all users possess identical copies of that blockchain and that no one person or authority has governing power over that blockchain or its uses. Developments and features are agreed on by way of reaching a majority consensus by its users.

The name, block + chain, hints at how it works.

What’s the ‘block’ in blockchain?

Every transaction is recorded and stored as a block of information. Each block is defined by a block-number and stores transaction data, including the transaction amount and a record of which wallets the transaction took place between. Each valid exchange of data results in a transaction ID - a unique code for each transaction. Securely possessing a ‘private key’ or password, users can ensure that their funds or digital items are accessible exclusively to themselves.

Each block is ‘mined’ or rather, cryptographically verified, to authenticate and validate the transactions occurring within that block. This process results in an ‘immutable’ (uneditable) database that is always available (decentralised) with all users certain they all hold the same verifiably correct information as all other users.

What’s the point of blockchain?

To businesses, organisations and individuals, blockchain:

- Removes the need for central points of data reliability

- Removes the use of unnecessary intermediaries or ‘middle men’

- Allows for “Trustless” behaviour and transactions

Becoming your own bank

Storing cryptocurrency requires that owners have some degree of technical knowledge. You have two options: a hot wallet or a cold wallet. Already lost? This in itself is a problem. Cryptonews has a great guide.

Each owner is responsible for their own ‘keys’, allowing them access to their cryptocurrencies or digital items. If the owner loses their keys then they will be unable to recover their digital assets. Though there are a growing number of services helping to recover or mitigate the loss of access to cryptocurrencies, lack of technical understanding when using technologies is still a large barrier to meaningful public adoption.

Though cryptocurrencies aren’t necessarily free from regulation (lawmakers and regulators have often played catch-up regarding new technologies), users are empowered to become their own ‘bank’ without censorship or authorisation by third parties.

What's the catch?

As news coverage peaked, ‘blockchain’ was still very much a buzzword, associated almost exclusively by-in-large with Bitcoin and other cryptocurrency projects skyrocketing in value. Back at the end of 2017, Bitcoin reached its highest value to-date. Online and above the line ads popped up all over the place, encouraging people to invest in cryptocurrency.

In June 2018, Google moved to banned cryptocurrency advertisements placed using the Google Ads platform on its ad platforms. This was due to a wave of scammers using their ad platforms to target people searching bitcoin related terms, sending them to lookalike (or altogether fake) websites and stealing their private keys and thus, access to their funds.their wallet information. The success of these scams demonstrated just how easy it was to fool people when it came to cryptocurrencies - and how impossible it was to address the crime. More recently, hackers infiltrated Twitter to send messages from blue tick verified accounts (those owned by brands and public figures), containing a link which promised to double people’s investment in Bitcoin but in reality just stole bitcoin.

Nevertheless, in addition to the problem of consumer understanding (or lack thereof), there are known technical issues - though, as a side note, all of which apply specifically to the use case of blockchain for cryptocurrency - and are not necessarily issues for other applications: Blockchain Hacking too, is a major problem. And because cryptocurrency is decentralised, stolen assets cannot be recovered - transactions cannot be undone by anyone.

Security challenges

Banks, for example, handle hundreds of thousands of transactions per second. At the moment, most cryptocurrencies can not. This, however, is not to say that scalability is impossible. Ethereum has already scaled to 100s of transactions per second and it’s next phase will enable an increase in transactions per second in the tens of thousands.

It’s not environmentally friendly

Operating a blockchain can require a huge amount of energy. This has been a huge criticism of Bitcoin, which requires the use of energy intensive hardware. However, it’s important to note that it isn’t the case for other applications of blockchain and that even in the case of Bitcoin, there are arguments suggesting that stacked up against alternatives, its environmental impact is unfairly exaggerated.

What are the applications of blockchain?

Yet regardless of whether blockchain is the future of monetary exchange, we’re still very much in the early stages of understanding its full potential. While the proliferation of startups using blockchain for blockchain’s sake, has damaged its image, in reality there are plenty of use cases for which the application of blockchain technology may well offer benefits. From supply chain management to healthcare records, we’re only at the very early stages of exploration. Blockchain won’t always be the answer. Its - arguably misguided - buzz may have diminished, but it’s not disappearing any time soon.

Getting insurance as a blockchain business

With new technologies comes new territories for insurers too. Some will shy away from these risks - or through lack of understanding, perhaps demand excessively high premiums. At Superscript, we’re different. We’re market leaders when it comes to our understanding of blockchain and crypto insurances and work with a number of innovative businesses in the blockchain space. Whatever technology your business is working with, our advised team is here to help you get the cover you need.

Find out more about Blockchain Insurance.

Related articles

This content has been created for general information purposes and should not be taken as formal advice. Read our full disclaimer.

We've made buying insurance simple. Get started.

- 15 November 20234 minute read

3 ways web3 companies can buy insurance

The risks web3 companies face are complex. With innovation at the forefront, it's important to ensure you're properly covered. Read on to discover the three main ways you can get the insurance you may need as a web3 innovator.

- 08 November 20234 minute read

The biggest risks web3 companies face

At Superscript, 100% of our web3 claims come from off-chain risks. As complex as the web3 landscape is, it’s often the places founders overlook that turn out to be the most important. Take a read of the three biggest risks web3 founders face.

- 06 September 20234 minute read

What new SEC cybersecurity rules mean for bitcoin miners

The Securities and Exchange Commission (SEC) recently announced sweeping changes to cybersecurity reporting that will have a profound impact. Are you prepared?